[1] Yukos CIS Investments Ltd [2] Wincanton Holdings BV Appellants/Claimants v [1] Yukos Hydrocarbons Investments Ltd [2] Fair Oaks Trade Invest Ltd [3] Glendale Group Ltd Respondents/ Defendants [4] Brittany Management Ltd Defendant

| Jurisdiction | British Virgin Islands |

| Judge | REDHEAD, J.A. [AG.],KAWALEY J.A. [AG.],Ian Kawaley,Michael Gordon, QC |

| Judgment Date | 26 September 2011 |

| Neutral Citation | VG 2011 CA 11,[2011] ECSC J0926-3 |

| Court | Court of Appeal (British Virgin Islands) |

| Docket Number | CLAIM NO BVIHC (COM) 85 of 2010,HCVAP 2010/028 |

| Date | 26 September 2011 |

IN THE EASTERN CARIBBEAN SUPREME COURT

IN THE HIGH COURT OF JUSTICE

CLAIM NO BVIHC (COM) 85 of 2010

Appearances: Mr Charles Hollander QC, Mr Philip Kite and Mr Stephen Midwinter for the Claimants

Mr Steven Berry QC, Mr Mark Forte, Mr James Willan and Ms Emily Wood for the First to Third Defendants

(Application for disclosure and freezing order or appointment of receiver and manager — respondents BVI companies — applicant asserting right to ownership of respondents' Dutch holding company in proceedings in Holland — applicant making no claim in BVI except right to have register of members of the respondents rectified — Rybolovleva v Rybolovlev considered — applicant relying upon Black Swan principle in support of claim to be granted interim relief — whether Black Swan applying in the circumstances — whether evidence of dissipation — whether appropriate to appoint receiver and manager — whether disclosure to be ordered)

This is an application by Yukos CIS Investment Limited (“Yukos CIS”) and its wholly owned subsidiary Wincanton Holdings BV (“Wincanton”) (bodies incorporated in the Republic of Armenia and in the Netherlands respectively and together “the claimants”) for orders (a) that the respondents Yukos Hydrocarbon Investments Limited (“YHIL”), Fair Oaks Trade and Invest Limited (“Fair Oaks”) and Glendale Group Limited (“Glendale”), three BVI incorporated companies, give detailed disclosure of (in short) their current financial condition together with details of their financial transactions from 30 September 2005 to date; (b) that the respondents' assets be frozen; and (c) that an interim receiver be appointed to each of the respondent companies to effect compliance with (a) and (b) and “to ensure that the business of the respondents is not conducted in a manner injurious to the interests of Yukos CIS or Wincanton.” Fair Oaks and Glendale are wholly owned subsidiaries of YHIL. The first to third defendants say that Brittany Management Limited, the party named as the fourth respondent, has “ceased to exist” and the claimants say that they are content to proceed against the first three respondents only (whom I shall refer to as “the defendants”). I shall say no more about the fourth respondent.

These proceedings arise out of the well-known break up of OAO-Yukos Oil Company (“Yukos Oil”). I do not think that it is necessary for me to go into the background to and reasons for that break up in any detail, other than to record (since Mr Steven Berry QC, who, together with Mr Mark Forte, Mr James Willan and Ms Emily Wood, appeared for the defendants in this application relied heavily upon the fact) that the conduct of the Russian Government in this matter has been condemned by the Parliamentary Assembly of the European Council and by Courts in England, Cyprus, Denmark, Lithuania and Spain. In addition, the European Court of Human Rights has declared the complaint of Yukos Oil admissible. A judgment of that Court is currently awaited. I may as well say at the outset that it does not seem to me that the rights and wrongs of the events leading up to the break up and sale of Yukos Oil have any bearing upon the issues which I have to determine on this application.

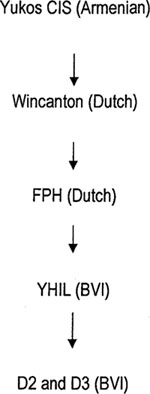

The essential facts for present purposes are that pressure built up on Yukos Oil in early 2004. In response, its principal subsidiary was auctioned off in December of that year. In May 2005, Mr Khodorkovsky, the principal behind Yukos Oil, was convicted of tax fraud and sentenced to eight years in prison. Seeing the net closing in, the management of Yukos Oil in September 2005 arranged that one of its subsidiaries, Yukos CIS 1, should transfer its own wholly owned subsidiary, YHIL, to Wincanton, another wholly owned subsidiary of Yukos CIS brought into existence for the purpose. Wincanton then transferred YHIL (and with it YHIL's subsidiaries Fair Oaks and Glendale) to Wincanton's Netherlands-incorporated subsidiary Financial Performance Holdings BV (“FPH”). The outcome may be represented thus:

It will be noticed that the effect of these manoeuvres was to create a structure in which two Netherlands incorporated companies stood back to back in the chain of ownership. This feature enabled Yukos Oil to take advantage of an entity known to the law of the Netherlands as a Stichting. As I understand, a Stichting is capable of holding property while itself being ownerless, rather like a human trustee. It issues what are called depositary receipts, which entitle the holders

to all the income passed up from the entities owned by the Stichting, but only at a time of the Stichting's choosing. Once the structure diagrammatised above had been put in place, Wincanton transferred its shares in FPH for no consideration to Stichting Administratiekantoor Financial Performance Holdings (“Stichting FPH”) in exchange for all of the depositary receipts issued by Stichting FPH. The effect, therefore, was that Yukos CIS ceased to have any control of its BVI subsidiaries, while retaining the ultimate right to be paid their profits—but only when the directors of Stichting FPH saw fit. At present, the directors are refusing to distribute income until the outcome of the present struggle for control of the BVI subsidiaries is decidedIt was a further feature of Stichting FPH that its original Articles forbade (put shortly) the use of any of its property in satisfaction of what may be described as claims based on the tax assessments which gave rise to the difficulties in which Yukos Oil found itself in 2004. It appears that the Articles were restated and amended in March 2008. The restriction was deleted from the Articles of Stichting FPH and instead shifted to the partnership agreement of the Delaware limited partnership which has since September 2008 been the holder of the depositary receipts (see paragraph [7] below). On the other hand, a new provision, introduced in the March 2008 restated and amended Articles, allows Stichting FPH, after provision for creditors' claims, but only with the consent of the holders of the depositary receipts, to make distributions to “shareholders of Yukos Oil in accordance with the applicable law and principles of reasonableness and fairness.”

Yukos Oil was declared bankrupt in August 2006 and on 8 August 2007 its trustee in bankruptcy held an auction of Yukos CIS. The successful (for all I know, the only) bidder was a Russian state controlled oil company called OJSC Rosneft (“Rosneft”). Yukos CIS was transferred to Rosneft on 13 August 2007, but as a result of proceedings taken in Armenia by the ex-Yukos Oil management to challenge the transfer, Rosneft was unable to appoint its own board of Yukos CIS until some time in 2009. The Armenian court has upheld the validity of the transfer, although there remain unresolved ancillary proceedings challenging (as I understand it) the right of the Armenian Registrar of Companies to have registered it.

As is obvious from this summary of events, Rosneft must have known when it purchased Yukos CIS of the structure which I have summarised above and that it could have no control over YHIL or its subsidiaries unless it could undo the interpolation in September 2005 of Stichting FPH. Further refinements designed to make the chain of ownership even more complicated and to prevent the assets of the BVI companies from being used to pay off debts in the bankruptcy of Yukos oil were introduced by the ex-Yukos Oil management of Yukos CIS in 2008 and 2009. They involve the interposition of a Delaware corporation, later converted into a Delaware limited partnership, to which the depositary receipts previously held by Wincanton were assigned. There is no need for me to set out the details of these later transactions. I should mention, however, as is obvious, that when they were carried out Rosneft had yet to appoint its own board to Wincanton, which it managed to do only after a decision of the Dutch Court in its favour on 10 May 2010.

The current position, therefore, is that Rosneft has drilled down as far as Wincanton in the chain, but needs to set aside the transfer of the FPH shares to Stichting FPH in 2005 if it is to establish control of YHIL and its BVI subsidiaries. In July of this year it commenced proceedings in Holland designed to achieve this object. On 7 July 2010 it obtained pre-trial attachment of the FPH shares. On 19 July it brought a claim seeking, among other relief, an order declaring that the transfer of the FPH shares by Wincanton to Stichting FPH in September 2005 was void.

Had the dealings which I have summarized above taken place under English law, there could have been little doubt that any successor board could have caused Wincanton to unwind the transaction as having been by way of gratuitous transfer giving rise to a resulting trust in its favour, which it would have been entitled as sole beneficial owner to enforce by requiring the re-transfer of the FPH shares—notwithstanding provisions in the Terms and Conditions of Administration of Stichting FPH 2 purporting to exclude any right of the holders of the depositary receipts to bring Stichting FPH to an end 3.

Evidence has been put in from Dutch lawyers 4 which suggests that the matter may not be so straightforward in the Dutch courts. Although expressed in civilian terms, much of the evidence for the claimants mirrors the reasoning set out in the preceding paragraph, but importantly it appears

To continue reading

Request your trial